دسته بندی ها

اسپیکر

اسپیکر حراجی

حراجی لپ تاپ

لپ تاپ هدفون

هدفونمحصولات پرفروش

-

لپ تاپ دل

تومان25.000.000

لپ تاپ دل

تومان25.000.000

-

اسپیکر مینی

تومان699.000

اسپیکر مینی

تومان699.000

-

اسپیکر رنگی

تومان2.000.000

اسپیکر رنگی

تومان2.000.000

-

اسپیکر شیانومی

تومان2.100.000

اسپیکر شیانومی

تومان2.100.000

-

اسپیکر جیبی

تومان450.000

اسپیکر جیبی

تومان450.000

گالری

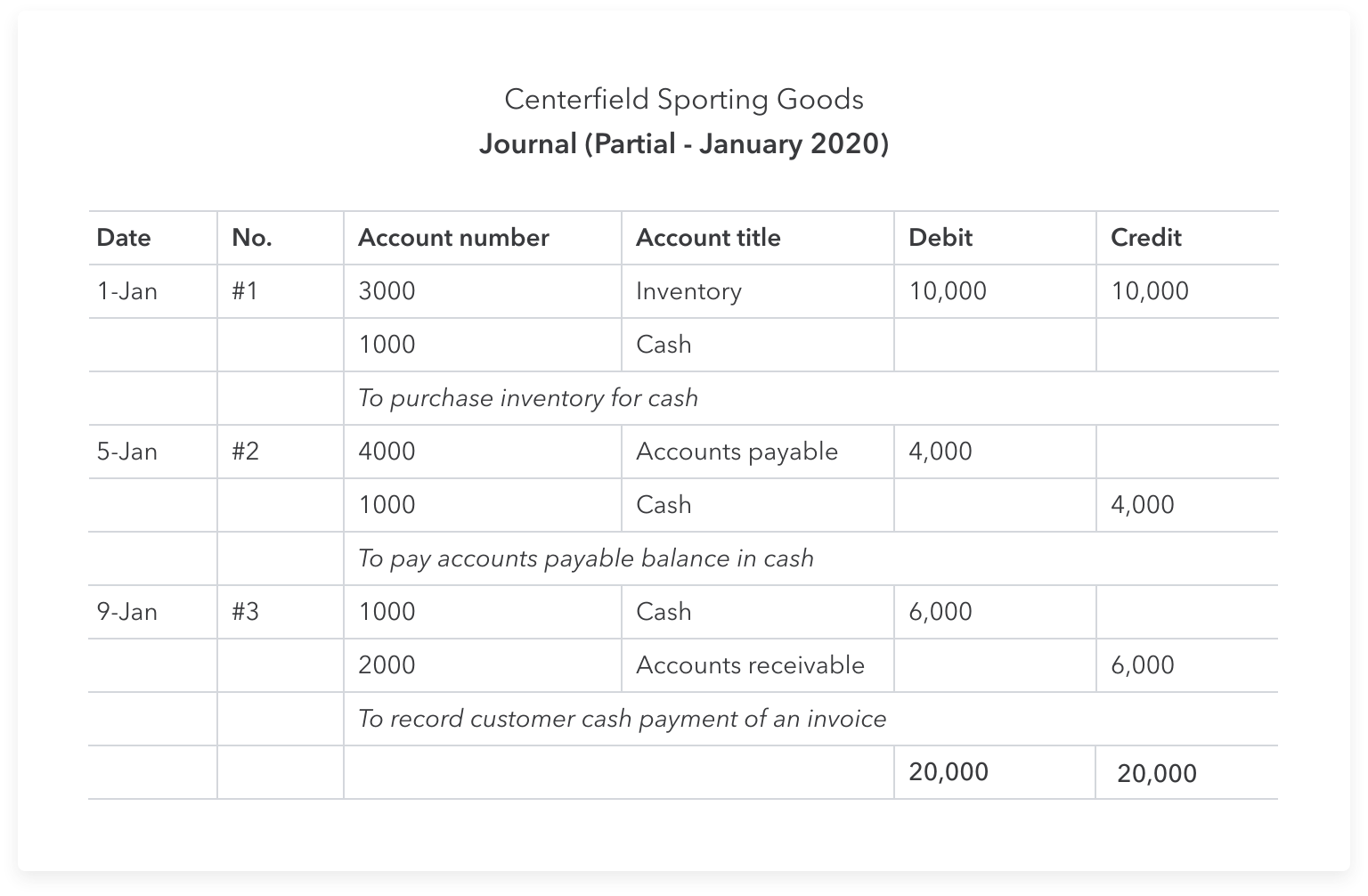

It simply deducts the inventory balance and increases the cost of goods sold balance. In this journal entry, the purchase of $5,000 does not add to the inventory balance but it will be used in the cost of goods sold calculation. The inventory balances will be based only on the physical count of inventory at the end of the period. Hence, unlike in the perpetual system, the company cannot check how much balances the inventory has immediately after adding the $5,000 of purchase on October 12, 2020.

How do you record an inventory purchase in accounting?

The method chosen for inventory valuation (FIFO, LIFO, Weighted Average) impacts COGS, which in turn affects gross profit and net income. Accurate inventory accounting ensures that COGS is correctly reported, leading to a true reflection of profitability. Incorrect inventory valuation can distort gross profit, operating income, and net income, potentially misleading stakeholders about the company’s performance. These examples highlight how inventory purchases impact a company’s accounting records, affecting both the balance sheet and cash flow, depending on whether the purchase was made in cash or on credit. The company needs to assess the inventory to provide an allowance of provision. It allows the company to record expenses before the inventory is actually written off, so the expense will spread over the financial statement.

How confident are you in your long term financial plan?

For instance, if inventory is purchased, there can be different entries depending on the business model. Like if inventory is purchased for further processing, it’s debited in the raw mater account and transferred to the working in process account. And once production is completed, it’s transferred to the finished goods account.

What Is AccountsBalance?

To understand perpetual inventory systems better, it is worth considering an example. Recently, computing systems and other input devices, networking technologies, and Internet-based applications have taken over and made perpetual how to value noncash charitable contributions inventory systems less burdensome for employees. Traditionally, the perpetual inventory system was used by companies that buy and sell easily identifiable inventories such as jewellery, clothing and appliances etc.

Additional entries may be needed besides the ones noted here, depending upon the nature of a company’s production system and the goods being produced and sold. Depending on your transactions and books, your accounts may look or be called something different. For information pertaining to the registration status of 11 Financial, please contact the state securities regulators for those states in which 11 Financial maintains a registration filing. In conclusion, these differences and many others highlight that it is wiser and easier to use a perpetual inventory system. By contrast, recording every single transaction as soon as it takes place is tiresome and monotonous for bookkeepers under a perpetual system, and so computers and other devices are used.

- This approach charges the cost of obsolescence to expense in small increments over a long period of time, rather than in large amounts only when obsolete inventory is discovered.

- Implement strong internal controls to ensure the accuracy and integrity of inventory adjustments.

- This system provides real-time inventory data, reducing the need for frequent physical counts.

- Suppose a manufacturing company purchased inventory at an original cost of $120k but now its market value has decreased to $100k from reduced customer demand.

- This transaction does not have any impact on income statement and balance sheet.

- So this actual damage will not impact income statement but the inventory reserve.

Inventory reserve allows the management to record expenses before the actual loss on the inventory. It helps management to allocate the inventory loss over its life and prevent the impact on any specific accounting period. When actual loss incurs, it will not increase additional expense as company already predicts and record the expense. In order to record inventory provision, we need to debit expense and credit inventory reserve which is the inventory contra account. Most companies use the cost of goods sold in the account to record this expense, but they may separate subaccounts for easy control.

When the expense account has been debited, the amount spent on the now obsolete inventory is shown as an expense. If you’re using a purchase account, add the balance of that account to the beginning inventory total, then subtract the costed ending inventory total to arrive at the cost of goods sold. Different categories of accounts are recorded on either side of the accounting ledger. Each transaction is recorded on both sides of the accounting ledger when the value increases and on the opposite side when the value decreases. Companies will either manufacture products to sell or purchase inventory from their suppliers.

Certified Public Accountants (CPAs) and other accounting experts can provide guidance on best practices, help navigate regulatory requirements, and offer solutions for challenging inventory issues. You report inventory obsolescence by debiting the relevant expense account and crediting the opposing asset account. An inventory write-off expense account records the value of any damaged inventory that cannot be sold. Inventory may be lost because of spoilage or other factors in the manufacturing process. Not all businesses use the raw materials inventory entry, but for those that do, it helps to track the cost of materials that move through a lengthy manufacturing process. To identify the amount of inventory purchased within a set timeframe you start with the total value of your beginning inventory, ending inventory, and of your COGS.

This integration ensures that inventory transactions are automatically recorded in the accounting system, reducing the need for manual data entry and minimizing the risk of errors. It also provides a seamless flow of information between inventory and financial records, supporting accurate financial reporting and analysis. Businesses should prioritize choosing software solutions that offer robust integration capabilities to maximize efficiency and accuracy. As well as recording your expenses, inventory accounting journal entries must also record your sales.

محصولات ویژه

دیدگاهتان را بنویسید